Gestão de Banca em Apostas Desportivas: Sistema Completo com Critério de Kelly

The most counterintuitive thing I tell bettors is this: your ability to size stakes correctly matters more than your ability to pick winners. I mean that literally. A bettor with a modest 3% edge who consistently stakes 10% of their bankroll per bet will go broke during a normal variance run before their edge ever has a chance to show up. A bettor with the same 3% edge who stakes 1-2% per bet will survive long enough for the math to work in their favor. Bankroll management is what converts a probabilistic edge into actual long-term returns. Without it, even correct analysis is self-defeating.

This is the framework I’ve refined over nine years: how to size a starting bankroll, how to determine what percentage to stake on each bet, the full Kelly Criterion formula with a worked example, and an honest comparison of flat betting, Kelly, and Martingale over a simulated run of 500 bets. The data here will make certain popular approaches look exactly as dangerous as they are.

Índice de conteúdos

- Por que a gestão de banca é mais importante do que escolher vencedores

- Quanto dinheiro precisa para começar: definir a sua bankroll inicial

- Dimensionamento das apostas: entre 1% e 5% por jogo

- Critério de Kelly: fórmula completa e exemplo passo a passo

- Flat betting vs. Kelly: comparação por simulação de 500 apostas

- Como criar e manter um diário de apostas eficaz

- Disciplina de banca em fases negativas: o teste real da gestão

Por que a gestão de banca é mais importante do que escolher vencedores

Most losses in the long run don’t happen because bettors lack sports knowledge — they happen because of poor bankroll management. That’s a hard claim to accept when you’re watching a match you know inside-out. It feels like knowledge should be the decisive variable. But consider the math.

Imagine two bettors with identical 5% edges — they correctly identify value bets that, on average, return 5% above stake. Bettor A stakes 2% of their bankroll per bet. Bettor B stakes 15% per bet, confident in their edge. Over 100 bets with normal variance — which includes runs of 8-10 losses in a row, a statistical inevitability at these odds — Bettor A’s bankroll barely notices the bad runs. Bettor B faces ruin risk before 50 bets. The runs don’t care about your edge. They’ll arrive on schedule regardless.

Sports betting without bankroll management is gambling. With bankroll management, it becomes a controlled statistical process. That distinction sounds abstract until you’ve watched a bettor with genuine analytical ability crater their bankroll because they overbet through a losing run and had nothing left when the variance corrected.

The psychological dimension matters too. Staking 15% of your bankroll on a bet means every result hits hard emotionally — wins produce overconfidence, losses produce panic. Both states corrupt decision-making. Staking 1-2% keeps individual results from feeling catastrophic, which in turn keeps your decision process calm and consistent. That emotional stability has measurable value over thousands of bets.

Quanto dinheiro precisa para começar: definir a sua bankroll inicial

A question I get constantly: “How much do I need to start?” The answer depends on two things: your minimum bet size and how many bets you expect to place per month.

The practical formula is simple. If you’re betting €10 minimum per selection, and you’re staking 2% per bet, your bankroll needs to be at least €500 (€10 ÷ 0.02). If you’re staking 1%, you need €1,000. The principle: your bankroll must be large enough that your percentage stake produces a bet size that the markets actually accept.

More importantly, your bankroll must be large enough to absorb the losing runs that will come without forcing you to abandon your strategy. A 15-bet losing run — not catastrophic by any statistical measure at odds around 2.00 — erodes a 2%-staking bankroll by 26%. That’s painful but survivable. The same run wipes out 70% of a 10%-staking bankroll. One bad month ends the entire project.

The standard professional recommendation is to start with enough bankroll that you could lose 20 consecutive bets and still have at least 60% of your original stake remaining. At 2% staking: (0.98)^20 = 0.668, or 66.8% remaining after 20 consecutive losses. That’s the floor of acceptable resilience. If your bankroll size doesn’t allow that margin, you’re betting too large a percentage, not too small a bankroll.

One more practical note: your betting bankroll should be completely separate from your living expenses. This isn’t a moral judgment — it’s a mathematical one. Mixing betting funds with money you need to live introduces emotional stakes that distort decision-making in ways that are hard to compensate for.

Dimensionamento das apostas: entre 1% e 5% por jogo

The industry standard, consistent across serious bankroll management analysis, is to bet between 1% and 5% of total bankroll per individual wager. Within that range, where you land should reflect the strength of your edge and the uncertainty in your probability estimates.

At the conservative end (1-2%), you preserve bankroll through extended losing runs and keep the psychological pressure low. The trade-off is slower growth during winning periods. At the aggressive end (4-5%), growth during winning runs is faster, but losing runs hit harder. For most recreational bettors — those placing 50-150 bets per month without a deeply validated model — 1-2% is the right range. It keeps the project sustainable long enough to develop skill.

A useful heuristic: increase your stake percentage only after demonstrating a positive ROI over at least 300 bets. Not 50 bets. Not 100 bets. Three hundred. Before that threshold, you’re in the noise zone — positive results might be variance, not skill. After 300 bets with consistent positive returns, you have meaningful evidence of genuine edge. That’s when incrementally increasing stakes makes mathematical sense.

One refinement worth making: vary your stake within the 1-5% range based on perceived edge strength. A bet you assess at 8% EV warrants a larger stake than one at 3% EV. This is essentially the logic of Kelly Criterion, which we’ll formalize in the next section. The important constraint is that your maximum stake — even for your highest-confidence selections — should never exceed 5% of current bankroll. The Kelly formula will sometimes suggest higher percentages; applying it at full Kelly is almost always a mistake in practice.

A specific trap worth naming explicitly: the “sure thing” exception. Every bettor eventually encounters a match they’re so confident about that normal stake sizing feels artificially timid. The conviction feels different from regular analytical confidence — it feels like certainty. This is precisely when discipline around maximum stake percentage is most important. The psychological state that produces subjective certainty is also the state most vulnerable to confirmation bias. The most costly individual losses I’ve experienced across nine years came on bets I felt certain about. The most consistent monthly returns came from rigorously applying 2% flat staking to selections I felt only moderately confident about. Certainty is not a reliable signal to increase stakes; it’s often a signal to recheck your analysis for overlooked contrary evidence.

Critério de Kelly: fórmula completa e exemplo passo a passo

The Kelly Criterion is the mathematically optimal bet-sizing formula for maximizing the long-run growth rate of a bankroll. It was developed by physicist John Kelly Jr. in 1956 and has been applied to everything from stock portfolios to sports betting ever since. Understanding it changes how you think about stake sizing permanently.

The Kelly formula:

f* = (bp – q) ÷ b

Where:

f* = the fraction of your bankroll to stake

b = the net odds (decimal odds minus 1)

p = your estimated probability of winning

q = your estimated probability of losing (1 – p)

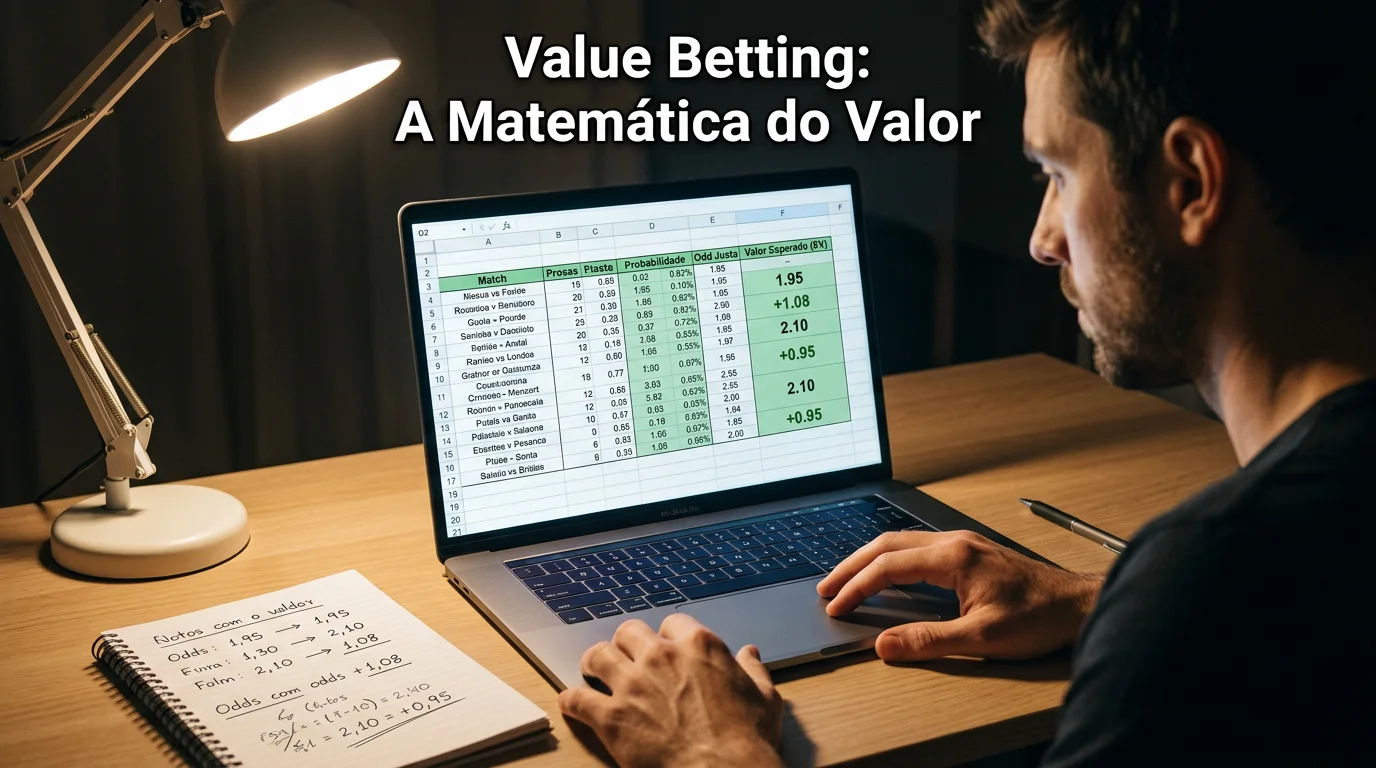

Worked example: You’re considering a bet on an away win priced at odds 3.50. Your analysis gives the away team a 35% chance of winning.

b = 3.50 – 1 = 2.50

p = 0.35

q = 0.65

f* = (2.50 × 0.35 – 0.65) ÷ 2.50 = (0.875 – 0.65) ÷ 2.50 = 0.225 ÷ 2.50 = 0.09

Full Kelly suggests staking 9% of your bankroll. On a €1,000 bankroll, that’s €90 on a single bet. That is extremely aggressive and I do not recommend it.

The standard professional practice is to use fractional Kelly — typically one-quarter to one-half of the full Kelly percentage. At half Kelly: 4.5%. At quarter Kelly: 2.25%. These fractions dramatically reduce volatility while preserving most of the long-run growth advantage. The research shows that half-Kelly produces about 75% of the growth rate of full Kelly, while reducing drawdown volatility by approximately half. That’s a compelling trade-off.

Why not full Kelly? Because the formula assumes your probability estimates are perfectly calibrated — that your 35% really is 35%, not 33% or 37%. In practice, all probability estimates carry uncertainty. When your estimate is off in the wrong direction, full Kelly punishes you severely. Fractional Kelly provides a margin of safety for estimation error without sacrificing much long-run performance.

Flat betting vs. Kelly: comparação por simulação de 500 apostas

Let me compare two approaches head-to-head on identical conditions: 500 bets at average odds 2.20, with a genuine 5% edge (true win probability 50%, implied probability 45.5%). Starting bankroll: €1,000.

Flat betting at 2%: Each bet is €20, regardless of outcome or perceived edge. Simple, predictable, psychologically manageable. After 500 bets with 5% EV, expected profit is approximately €500 — a 50% return on initial bankroll. Maximum drawdown in typical variance runs: around 18-22% of bankroll. This approach is far more common among successful recreational bettors than models suggest it should be.

Half-Kelly: Stake varies between 1% and 5% based on edge strength, averaging around 2.5% for a consistent 5% edge. After 500 bets, expected profit is approximately €620 — a 62% return. Maximum drawdown in typical variance runs: around 23-28% of bankroll. The higher average stake produces better returns but with more volatility.

The conclusion from this simulation isn’t that one method is universally superior. It’s that both are viable, and Martingale is not in the comparison because Martingale fails categorically. A Martingale system — doubling stakes after each loss — produces apparent stability in the short term while accumulating catastrophic ruin risk. A run of 10 consecutive losses starting from a €10 base stake requires a bet of €10,240 on the 11th selection. Most bettors hit their bankroll or operator limit long before the system “recovers.” The expected value of a Martingale system over thousands of bets is deeply negative; it works until it doesn’t, then it wipes you out completely. For a dedicated analysis of exactly why, see the breakdown of Martingale in practice.

The practical recommendation: start with flat betting at 2% until you have 300+ bets of verified positive ROI. Only then consider moving to fractional Kelly, and only at one-quarter Kelly initially. This progression matches the accumulation of evidence about your actual edge, not your assumed edge.

Como criar e manter um diário de apostas eficaz

Every professional bettor I’ve spoken to keeps records. Not because they’re meticulous by nature — most aren’t — but because after one painful experience of not knowing whether a losing run reflects bad process or bad luck, they never skipped records again.

The minimum viable bet log has seven fields: date, competition, match, market, odds, your estimated probability, and outcome (win/loss/push). With those seven fields, you can calculate ROI by market type, by competition, by estimated probability range, and over time. Those breakdowns reveal more about your betting than any other analysis you could do.

The most valuable insight a betting log provides is calibration data: are your 60% estimates winning 60% of the time? Are your 40% estimates winning 40%? If your 60% estimates are winning only 50%, you’re systematically overconfident — your model is producing estimates that are too high. If they’re winning 68%, you’re underconfident in your estimates and leaving value on the table by staking conservatively. Without a log, you’re flying blind on the question that matters most: whether your probability estimates are accurate.

Review your log monthly, not weekly. Weekly reviews introduce too much noise — a single good or bad run can dominate. Monthly reviews with 40-80 bets give you a more meaningful signal. The questions to ask: Which markets is my ROI positive in? Which is it negative? Is there a pattern in which probability ranges I’m miscalibrating? Has my ROI changed in the last three months compared to the three months before? That last question is the early warning system for when markets are adjusting to your betting patterns or when your methodology needs updating.

Beyond the standard fields, there are three additional data points that most bettors overlook but that dramatically increase the analytical value of a log. First: record your estimated probability before you look at the bookmaker’s odds. This forces the habit of independent probability assessment and gives you calibration data. Second: record the time of bet placement relative to kick-off. Bettors who routinely bet in the final two hours before a match often do so under time pressure and with less thorough analysis; if your early-week bets consistently outperform your match-day bets, that’s a structural signal to change your workflow. Third: record your emotional state or confidence level with a simple 1-5 rating. If your 5/5 confidence bets are consistently underperforming your 3/5 bets, you’ve identified overconfidence as a specific problem to address.

The tools for bet tracking range from a simple spreadsheet — entirely adequate for most bettors — to dedicated applications. The platform matters less than the consistency. A spreadsheet you update religiously beats a sophisticated app you forget to fill in after losses. The one technical feature worth seeking in any tracking system: automatic ROI calculation segmented by market type. Manual calculation of market-specific ROI is tedious enough that most people stop doing it; if your system does it automatically, you’ll actually look at the data.

Disciplina de banca em fases negativas: o teste real da gestão

The true test of any bankroll management system isn’t how it performs when you’re winning — it’s how it performs and how you respond when you’re not. I’ve been through losing runs of 18 consecutive bets on selections I remain convinced were genuinely value. Those runs are statistically unremarkable — they’re part of the distribution. But the temptation to respond to them by changing something, anything, to stop the bleeding is profound.

The response protocol I use during negative phases: first, review the last 20 bets against the original criteria — was each bet genuinely positive EV by my model, or did I force some of them? If the honest answer is that several bets were marginal, the losing run is partly a process signal. Tighten the criteria and move forward. If all 20 bets met the standard, the run is pure variance. Do not change anything. Continue with exactly the same methodology and stake sizing.

What you must never do during a losing run: increase stake size to recover faster. This is the logic that converts a temporary drawdown into permanent bankroll damage. At 2% flat stakes, a 20-bet losing run reduces your bankroll to approximately 66.8% of its starting value. Painful. But recoverable — it requires a 50% recovery from that depleted base. If you’ve responded to the run by increasing to 5% stakes in frustration, a five-bet losing extension reduces you to 60.5% of the depleted base, and you now need a 65% recovery. The mathematics of compounding losses punishes stake escalation severely.

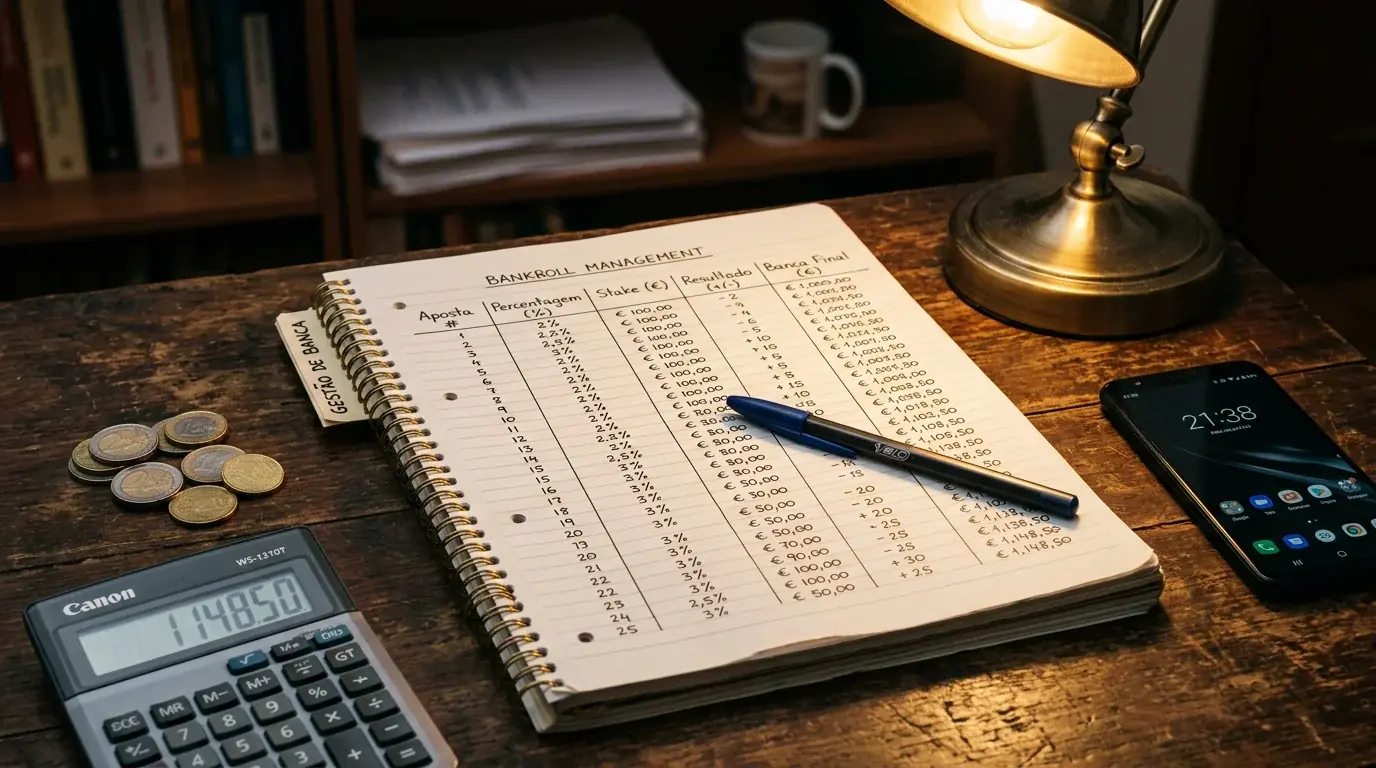

The concept of “units” helps here. Many bettors find it psychologically easier to track results in units (1 unit = 2% of starting bankroll) rather than euros. A unit-denominated log makes the mathematics more abstract and the emotional impact of individual results lower. A loss of 1 unit feels different from a loss of €50, even if they’re the same thing. That psychological distance is not irrational — it’s a practical tool for keeping decision quality high when results feel personal.

The final thing to understand about bankroll management is that it’s an ongoing calibration, not a fixed system you set once. As your bankroll grows, your absolute stake sizes grow, which can introduce new psychological dynamics — a €100 bet at 2% of a €5,000 bankroll feels different from a €20 bet at 2% of a €1,000 bankroll, even though the mathematics are identical. Some bettors become more conservative as stakes grow, which suppresses returns below their optimal level. Others become more aggressive, abandoning the percentage discipline that produced the growth in the first place. Recognizing which direction your behavior drifts and correcting for it is part of the ongoing management the system requires.

Periodically — every six months is reasonable — review your stake sizing relative to your current bankroll and your current demonstrated ROI. If your ROI is positive over 300+ bets and your bankroll has grown substantially, a modest increase in your percentage stake (from 2% to 2.5%, for example) is mathematically justified and may be appropriate. If your ROI has turned negative over the last 200 bets, a reduction in stake size is the correct response — not to “protect” the bankroll emotionally, but because declining ROI is a signal that your edge may have narrowed and your optimal Kelly fraction is lower than it was. The goal of bankroll management, ultimately, is keeping you in the game long enough for your edge to express itself. Everything in this framework — from the percentage calculations to the record keeping to the variance awareness — serves that single function.

Qual é o tamanho ideal de bankroll para começar a apostar?

Não há um valor único, mas a regra prática é esta: a tua bankroll deve ser suficientemente grande para que 2% da mesma produza o tamanho mínimo de aposta que pretendes colocar. Se apostas mínimo €10, precisas de €500 de bankroll para apostar a 2%. Se apostas mínimo €25, precisas de €1,250. Mais importante: a bankroll deve suportar 20 perdas consecutivas e ainda reter 60% do valor original.

Como o Critério de Kelly difere do flat betting em termos de risco?

O flat betting oferece volatilidade previsível e menor drawdown máximo, ao custo de não ajustar o tamanho das apostas ao nível de confiança. O Kelly ajusta as apostas ao EV estimado, gerando retornos potencialmente superiores, mas com maior volatilidade de curto prazo. Para a maioria dos apostadores sem um modelo altamente calibrado, o flat betting a 1-2% é mais seguro e igualmente eficaz a longo prazo.

Devo usar Kelly completo ou Kelly fraccional?

Quase sempre fraccional. O Kelly completo assume estimativas de probabilidade perfeitas, o que nenhum apostador tem. Ao usar a fórmula a 100%, qualquer erro de estimativa amplifica as perdas significativamente. O Kelly fraccional a um quarto ou metade do valor calculado preserva a maior parte do crescimento de longo prazo enquanto reduz o risco de ruin a metade.

O sistema Martingale funciona em apostas desportivas a longo prazo?

Não. O Martingale cria a ilusão de segurança ao converter pequenas perdas frequentes em grandes perdas raras. Matematicamente, o risco de ruin é 100% com bankroll finita. Uma sequência de 10 perdas consecutivas — estatisticamente provável em qualquer amostra longa — exige uma aposta de 1.024 vezes a aposta inicial, o que excede os limites de bankroll ou de operador da grande maioria dos apostadores.

Criado pela redação de «Dicas de Apostas Desportivas».